I’m sure many people have heard the term GAAP used in one conversation or another, but unless you are a seasoned accounting or finance professional, you might know little about these important regulations, besides what the acronym stands for.

In this article, I hope to shed light on some well-known and lesser-known facts about GAAP and also discuss how accounting and finance software can help organizations stay compliant with GAAP while improving the efficiency and speed of creating financial statements.

What is GAAP?

Generally accepted accounting principles (GAAP) are a set of rules and regulations that public companies in the US must follow when their accounting teams create and update their financial statements.

The purpose of these rules is to improve the transparency and consistency of financial reporting and ensure consistency between organizations.

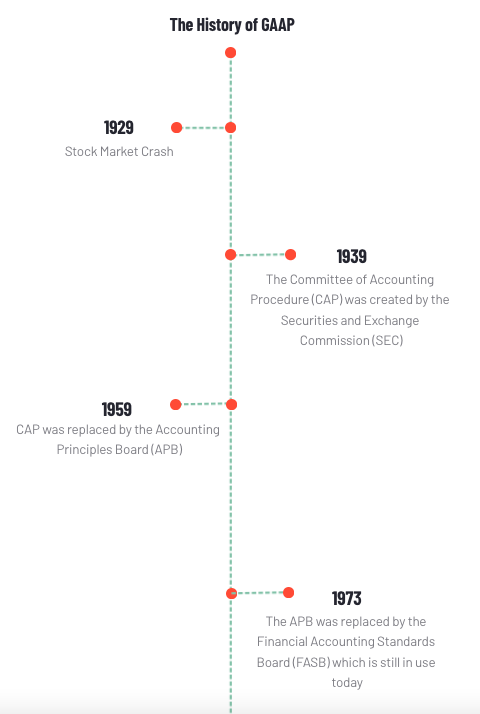

The history of GAAP

Let’s go back to the stock market crash of 1929, at the beginning of the great depression. At this time, the US government had deemed it necessary to regulate the accounting practices of publicly traded companies because it was believed that many of these organizations had less-than-honest accounting standards and practices, which partially led to the crash.

Authority was then given to the Securities and Exchange Commission (SEC) to create a common set of accounting standards, and therefore, 10 years later in 1939, the Committee on Accounting Procedure (CAP) was created. Twenty years after this, CAP was replaced by the Accounting Principles Board (APB), which started releasing suggestions about what major accounting standards and principles should be adopted by accountants of publicly traded companies. In 1973, the APB was replaced by the Financial Accounting Standards Board (FASB), which is still present today, and continues to issue accounting opinions and render judgments. Did you get all that? Good.

Why is GAAP important?

GAAP is important for both consumers and companies. GAAP helps instill trust in companies by thwarting the manipulation and modification of financial information, which can easily change the perception of a company.

Having consistent accounting standards across the board helps ensure trust in the financial markets. If investors were hesitant to trust the information presented by companies they were invested in or considered investing in, they would have less confidence in the integrity of that company and be less likely to invest. It also allows companies to gain further insight into their performance and minimizes the chance of errors in reporting by having safeguards in place.

The core principles of GAAP

There are 10 major principles of GAAP that serve as the foundation of accounting and emphasize the backbone of the guidelines public companies need to follow. They're listed below:

- Consistency: Consistent standards and methods are followed in reporting from period to period.

- Regularity: All accountants adhere to and follow the rules and regulations set forth by GAAP.

- Permanence of method: Consistent procedures are used in the creation of financial reports.

- Noncompensation: Whether a company’s financial outcome is positive or negative, all aspects are fully reported.

- Sincerity: Accountants will create and share financial reports accurately and honestly.

- Periodicity: Standard, commonly accepted time periods, such as quarters and years are used for reporting.

- Materiality: All financial reports clearly and fully disclose an organization's financial situation.

- Good faith: Anyone involved in the financial reporting process will act honestly and in good faith.

- Continuity: The valuation of assets within a company is based on the assumption that the business will continue to operate as normal moving forward.

- Prudence: Speculation will not be used to influence the reporting of financial data.

The equivalent of GAAP for countries outside of the US

Outside of the US, the International Financial Reporting Standards (IFRS) exists. It is regulated by the International Accounting Standards Board (IASB) and is the official accounting standard in the European Union and more than 140 jurisdictions worldwide. While GAAP and IFRS are both accepted guidelines of accounting for their respective countries, they do have their differences. Presumably, the biggest difference between the two is that IFRS is more of a principle-based accounting standard, while GAAP is more rules based. So what does that mean?

Principle-based accounting requires that companies following this system comply with a set of accounting principles. If not, they must provide a reasonable explanation as to why they strayed from these principles. This accounting practice allows accountants to use their professional judgment and interpretation when reporting financial information but requires a tremendous amount of disclosures.

On the other hand, GAAP uses rules-based accounting which follows a standardized process for reporting financial statements. Companies and their accounting teams must comply with these rules when compiling financial statements, which allows stakeholders to compare financial data from different organizations. This style of accounting sets rules that need to be obeyed in every situation which can restrict accountants from applying their professional interpretation and skepticism.

Another important difference between the two accounting standards is regarding inventory methods. Under IFRS, LIFO, or last in first out, is not used, while GAAP prefers this method. IFRS standards are opposed to LIFO because it’s possible to understate a company's earnings to keep taxable income low, and can also result in inventory estimations that are obsolete. On the other hand, GAAP approves of LIFO because it matches current costs with current revenue and theoretically makes income statements and balance sheets more accurate.

What is non-GAAP?

Non-GAAP accounting is any type of accounting in the US that is not GAAP and does not follow a set of standards. Because financial statements created under GAAP guidelines can be difficult to understand based on their format, both public or private companies sometimes use non-GAAP accounting practices to make their financial statements easier to understand for investors and other stakeholders.

Organizations also use non-GAAP accounting practices to paint a clearer picture of business operations by excluding non-recurring expenses, such as big-ticket items. Companies may use non-GAAP accounting as long as their statements are disclosed and reconciliation is provided between the regular and adjusted results.

The role of accounting software with GAAP

Accounting software for both enterprise and SMB companies can help them follow GAAP guidelines by assisting in the entry and processing of financial data and statements. Reconciliation of general ledger (GL) accounts is necessary to ensure that financial information is reliable and to identify and correct any fraudulent or unusual activity.

Accounting software assists in organizing this data to ensure that credits and debits are recorded in the correct places so when a bookkeeper or financial controller sits down to review the data, they can spot anything that seems out of place or unusual. Some accounting software also have features from accounts payable (AP), accounts receivable (AR), invoicing, and payroll processing, which help companies stay consistent with GAAP and tax guidelines.

Other accounting and finance software are readily available for not only the creation and presentation of balance sheets, income statements, and cash flow statements, but to prepare for audits, and the month, quarter, or year-end financial close process. Financial audit software ensures companies comply with both internal and external regulations to maintain GAAP or other compliances, reduces fraud, and identifies suspicious activity that may affect a company’s bottom line.

Financial close software is used during the financial close process to ensure the books are accurate and all transactions were completed. Financial close products often include additional features such as individual task allocation, reconciliation management, reporting, and databases of past accounting close data organized by month and transaction type. All of these attributes help companies stay within GAAP regulations and ensure all financial reports are accurate.

| Related: How to Stay Organized When Closing Books Remotely → |

On G2, users can search, filter, and compare hundreds of accounting and finance software and services that can help them govern and oversee their accounting processes. Users have left many reviews about accounting & finance software that have helped them manage their accounting processes and stay within GAAP guidelines.

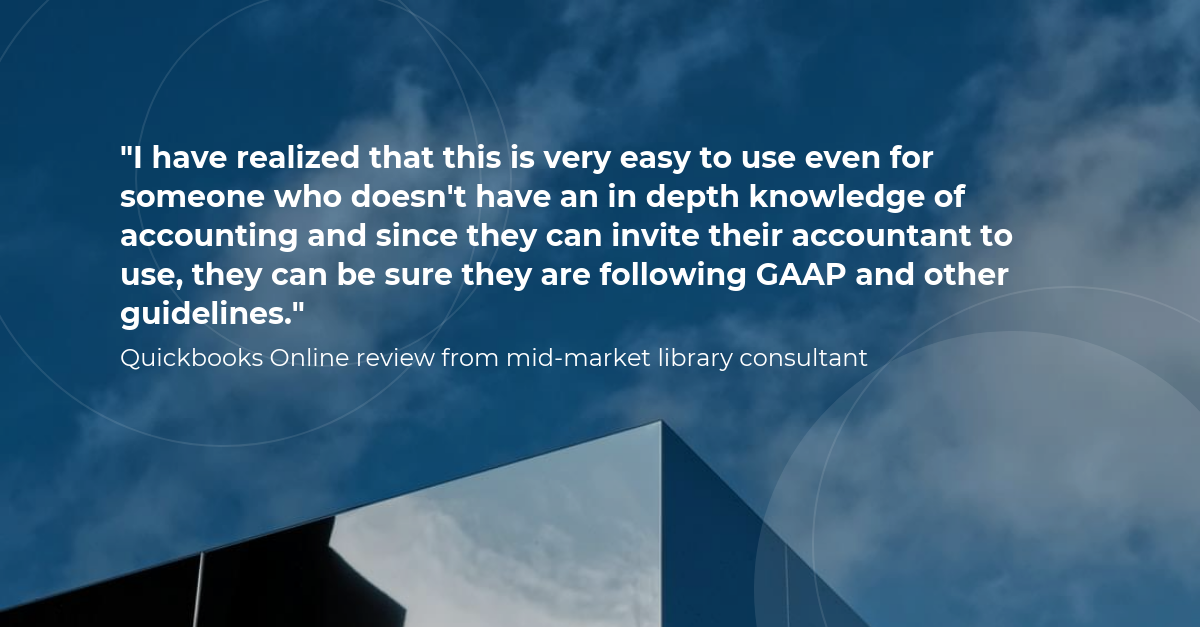

A mid-market library consultant left this review about Quickbooks Online:

When a systems administrator in the chemical industry was asked about what problems they are solving and what benefits they have realized with Planful, a financial close software, they answered.

“It allows us to be flexible with management reporting (different business units, etc.), while maintaining GAAP consolidated reporting.”

There’s no doubt that a standardized set of regulations and guidelines are necessary to ensure that financial reporting is consistent and comparable for both consumers and companies. Even though only publicly traded companies are required to use them, small business owners and managers should understand GAAP to decide whether to implement the principles within their accounting practices. Either way, advancements in accounting & finance software can help these teams better understand and manage their finances to stay compliant with GAAP guidelines.

Want to learn more about Accounting Software? Explore Accounting products.

Nathan Calabrese

Nathan is a Senior Research Analyst at G2 focusing on finance and accounting software and their respective markets. Coming from the world of finance, Nathan understands and is familiar with the importance of finance/accounting software, and the complexities, struggles, and nuances that come with them. He has over 15 years of analytical experience in industries ranging from health care and transportation logistics to food service and software. Nathan received his MBA in finance and international business administration from the University of Illinois, Chicago, and his B.S. in production and operations management from California State University, Chico.